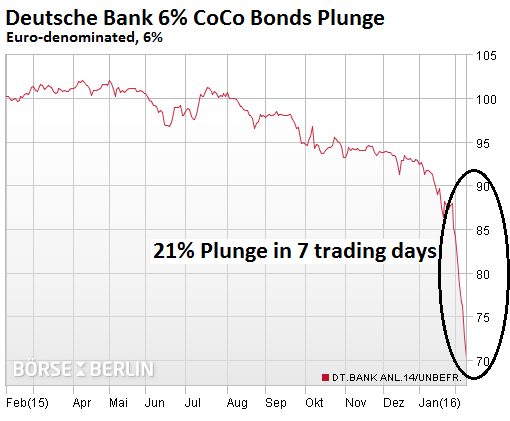

True enough, and a good clarification. However, it points to a bigger problem - if you, the buyer, are getting 6-8% for loaning DB money and I, the secondary market want 16% to take that bond off your hands, you're not making money. More than that, DB has a helluva time continuing to sell CoCos. From my understanding, CoCos amplify risk an outsized amount compared to their value because they have that magic "DB hits 12 poof you own stock" aspect. Worse than that, DB doesn't have to count the stock that goes poof until it goes poof, which means it also dilutes the fuck out of shares when it blows up. So it's not just that they're risky, it's that they externalize that risk to everyone else that holds DB, whether or not they own CoCos. There's a built in "cascade of bullshit" with convertibles in general but it's been held in check somewhat by the fact that the conversion is usually a litigation point. With CoCos that conversion point is writ in stone, which makes it rip quick and relentless. Finally, these are bonds that are being traded at 16% in an environment where nothing trades at 16%. Every trader I follow has been bitching about yields and how boring the market is these days and I think you, yourself pointed out that the problem with addiction to high-yield financing is that when the yield drops the cost of business spikes (can't find the comment, though). So the guys that are buying into CoCos aren't doing it on a lark, they're doing it because they've been painted into a corner by an environment where it's a stone bitch to make money. And now poof they're shareholders. In a failing asset. That they sure as fuck wouldn't have bought back when it was healthy; not without those 16% yields, anyway. And when the bonds convert, and the stock dilutes, and the share price has already been plummeting, it's gonna get messy on more than the guys holding the CoCos. It's gonna get messy on the guys that know the guys that know the guys that do business with the guys that hold the CoCos.